A secure retirement rarely relies on a single source of income. Most people build their retirement lifestyle from a combination of pensions, State entitlements, savings, property, and sometimes part-time work. Understanding how these income streams interact is the foundation of good planning.

The State Pension

Provides a guaranteed income (~€15,000 per year for full contributory rate).

Paid for life and broadly inflation-linked.

Forms the essential baseline but is rarely sufficient on its own.

Case Study – State Pension as the Core

Brigid qualifies for the full contributory State Pension (€15,000). With €5,000 from savings, her total = €20,000/year. It covers essentials but leaves little for travel or leisure.

Employer Pensions

Employer pensions usually provide the largest supplement to the State Pension.

Defined Benefit (DB)

Formula-driven (typically 1/80th pension + 3/80ths lump sum per service year). Offers secure, predictable income.

Defined Contribution (DC)

Value depends on contributions and investment growth. Flexible but uncertain.

Case Study – Dual Career Couple

Michael (public sector DB pension €22,000/year + €60,000 lump sum).

Niamh (private DC: €300,000 fund → ARF €225,000, lump sum €75,000).

Together with 2 State Pensions (~€30,000), annual retirement income = potentially €62,000 plus lump sums.

Private Pensions & AVCs

PRSAs and Personal Retirement Bonds allow additional saving

AVCs (Additional Voluntary Contributions)

Tax-relieved top-ups.

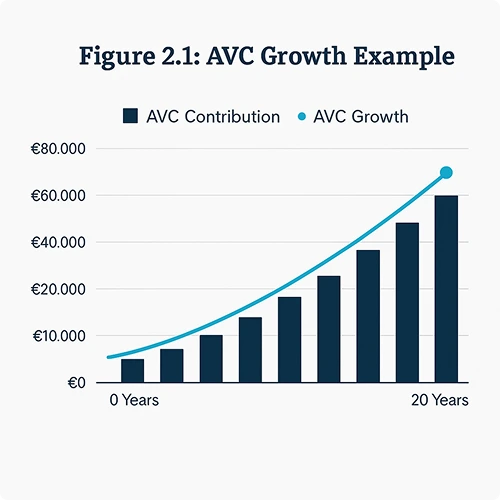

Example – AVC Boost

John contributes €500/month AVCs for 15 years.

At 4% growth → ~€120,000 fund, providing €6,000/year income or boosting his lump sum.

Savings & Investments

Accessible and liquid, but taxed heavily (DIRT, CGT) and vulnerable to inflation.

Example – Managed Drawdown

Anne has €100,000 in savings. Withdraws €5,000/year. If invested at 3% growth, it supports ~€6,700/year for 20 years.

Property Income

Rental income provides steady cash flow.

Rental income provides steady cash flow.

Case Study – Downsizing

Eamonn and Deirdre sell their home (€800,000) → buy smaller (€500,000). They free €300,000, invest proceeds, potentially generating additional income but will be subject to the appropriate taxes (eg Income, CGT, Exit tax).

Work & Business

Many retirees work part-time for income and purpose.

It’s becoming an increasing phenomenon

Example – Phased Retirement

Patrick, 67, earns €20,000 part-time. Delays ARF withdrawals, giving his pot more time to grow and also giving him some purpose as he wasn’t ready to stop working altogether.

Inheritances or Windfalls

While not reliable, inheritances can significantly impact retirement finances.

Key Takeaway

The most resilient retirement incomes are diversified: secure (State + DB), flexible (DC/ARF, savings, property), and optional (work, inheritance).